Russia's Mining Registry (FNS): Step-by-Step Guide and Our Experience

How to join the Russian FTS crypto mining register: documents, deadlines, taxes, reporting and regulatory risks. Step-by-step guide with dashboard screenshots.

The FTS crypto mining register is not a mere formality or a one-off checkbox — it is the entry point into the legal mining regime for companies and sole proprietors. Until a business is entered into the register, its mining activity does not meet the requirements of the law. Once registered, a miner becomes transparent to the Federal Tax Service (FTS), banks and counterparties: it declares income, reports the digital currency it has mined, and operates within a regulated perimeter.

Important: specific dedicated fines and criminal liability for illegal mining are not yet in force as final law in 2026 — they are being discussed at the draft-bill stage. This does not mean there is no risk: grey-zone mining can still trigger general tax, energy, administrative and criminal-law mechanisms wherever the elements of an offence are present.

Plugging an ASIC miner into a socket and forgetting about it is no longer a business model. Once dedicated regulation appeared, mining became an activity to which the state applies clear requirements: registration, reporting, tax accounting, compliance with territorial bans, and operating through a correct legal structure.

In this post — how registration in the FTS register actually works, who is required to join it, what to check before filing an application, and how we, NODA, support this process for clients.

How we got into the register — our own experience

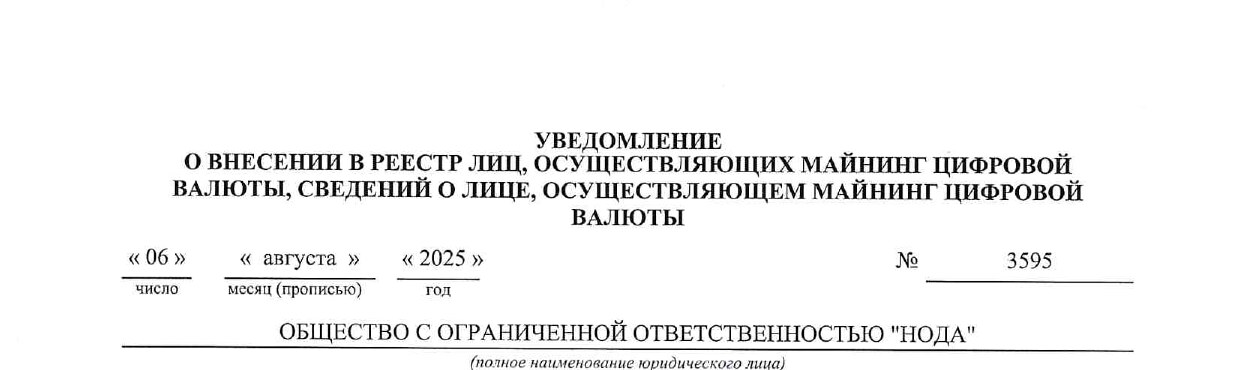

Before explaining how it all works, let us show you that we have been through it ourselves. Here is our notification from the FTS:

Confirmation from the FTS register: NODA LLC, record No. 7102500001895, date of entry — 06.08.2025.

From this moment, information about NODA LLC has been entered into the relevant FTS register. We operate within a regulated perimeter and support clients on equipment hosting, data and document preparation, and interaction with the FTS within the chosen cooperation model.

It is important to separate the roles: if the client is itself a miner and taxpayer, its registration, tax and reporting obligations do not disappear automatically. If a mining infrastructure operator is involved in the project, its role and powers must be set out separately in the contract. The specific model is always documented.

What the FTS mining register is and why it appeared

In August 2024, Russia introduced dedicated regulation of mining. Federal Law No. 221-FZ of 08.08.2024 amended Law No. 259-FZ and other acts, establishing the concepts of digital currency mining, mining pools, mining infrastructure, mining infrastructure operators and the registers.

Before that, the industry long lived in a grey zone: mining was technically possible, but businesses still had open questions about taxes, banks, documents, proof of the origin of digital currency and dealings with counterparties.

The logic is now different: if a Russian legal entity or sole proprietor engages in mining, it must be entered into the FTS register. There is a separate register of mining infrastructure operators. These are two different registers and must not be confused. The FTS maintains both registers in the manner established by the Russian Government.

In plain terms. Before regulation, mining was like a business with no clear sign on the door: the equipment runs, digital currency appears, but for a bank, a tax inspector or a counterparty many questions remain. The register is a way out of the grey zone: you show who is mining, where the equipment is located, how the mined digital currency is accounted for and who is responsible for reporting.

Digital currency is now property — what that means in practice

For the purposes of the Russian Tax Code, digital currency is recognised as property. This means that receiving digital currency through mining, and any subsequent transactions with it, have tax consequences.

At the same time, it is important not to confuse things: digital currency is not legal tender in Russia and is not equivalent to money in a bank account. Its legal regime is a special one.

In plain terms. Previously, for many people bitcoin looked like "something digital" that was unclear how to handle in accounting and taxes. Now, for tax accounting it is an asset for which you must determine income, value, expenses and the tax base.

Mined some BTC — this counts as income on the date the cryptocurrency is received. Income is not determined by a "Central Bank rate for bitcoin", because no such rate exists. Mining income is determined based on the market quotation of the digital currency on the date the income is recognised. If the quotation is expressed in a foreign currency, it is converted into roubles at the official Central Bank of Russia rate on the relevant date. In other words: first we look at the market quotation of the digital currency, then we convert the value into roubles under the rules of the Tax Code.

Who must join the register and who does not

- Legal entity. A Russian legal entity — for example an LLC or JSC — that engages in digital currency mining must be entered into the register regardless of the amount of equipment.

- Sole proprietor. A sole proprietor who engages in digital currency mining must likewise be entered into the register regardless of the amount of equipment.

- Individual. A Russian citizen who is not a sole proprietor may mine without joining the register if the energy consumed by such activity does not exceed 6,000 kWh per month. The income must still be declared in the established manner.

In plain terms, with examples:

- A single Antminer S21 Pro consumes about 3,510 W. At 730 hours per month, that is roughly 2,560 kWh per month. A single unit owned by an individual usually fits within the limit.

- Two S21 Pro units — about 5,120 kWh per month, still within the 6,000 kWh limit.

- Three S21 Pro units — already about 7,680 kWh per month. The limit is exceeded.

Attempts to artificially split a farm between relatives, friends or different account holders may be assessed critically by regulators if the equipment in fact operates as a single mining complex. So one must look not only at the "paperwork", but at the real model of ownership, location, electricity consumption and income.

Where mining is prohibited: restricted territories

In December 2024, the Russian Government approved a list of territories where digital currency mining — including participation in a mining pool — is prohibited. The relevant act is RF Government Decree No. 1869 of 23.12.2024.

The list of territories and the timing of the ban must be checked against the current version of the decree. The ban is imposed not only on individual regions of Russia but also on specific territories within regions. In addition, in some regions the restrictions may be seasonal.

In plain terms. The logic here is not that "crypto is disliked". The logic is infrastructural: in a number of regions the power grid cannot handle the additional load, especially at peak times. Mining consumes a lot of electricity, and the state restricts it where this could create a deficit or accident risks.

As of 20 May 2026, Perm Krai is not among the territories where digital currency mining is prohibited. But the list may change, so it must be re-checked before launching a project.

Our site is located in Perm Krai, in the Ust-Kachka rural settlement, on our own gas-fired power generation. If your equipment is currently located in a region with restrictions, or you want to move mining into a clearer legal perimeter, we can offer equipment hosting and support with the organisational side. For B2B investors there is a turnkey data centre format: a dedicated site, an energy model, equipment hosting and project support within a single perimeter.

Step-by-step registration in the FTS register

Below is the basic logic of working through the FTS "MiningRegister" service.

Important: the interface and the set of information differ depending on who files the application — a person engaged in digital currency mining, or a mining infrastructure operator. Below we describe the general logic, but the exact set of fields and documents must be checked against the chosen status.

If you do everything yourself — follow the steps below. If you host equipment with us — we support your preparation and the filing of documents.

Step 1. Find the "MiningRegister" service on the FTS website

On the home page of nalog.gov.ru go to the "Services" section and find "MiningRegister". The service is also available directly at rmo.nalog.gov.ru — a single window for working with the mining registers.

The service has different scenarios for miners and for mining infrastructure operators. So before you start filing, it is important to correctly determine your status. The FTS states that the register of persons engaged in digital currency mining includes information on a sole proprietor or a Russian legal entity engaged in mining, including participation in a mining pool.

Step 2. Log in with an electronic signature

A qualified electronic signature is required to log in. In plain terms, a QES is a digital tool with which a company, sole proprietor or representative confirms a legally significant action.

The application must be signed with the QES of the applicant, or with the QES of an authorised representative who holds the proper authority. You cannot simply "file on the client's behalf with your own signature" without a correct legal structure and confirmation of authority.

If a mining infrastructure operator files the application on behalf of a miner, the contract between the miner and the operator must expressly provide for the operator's right to sign and submit such an application. That agreement is attached to the application.

Source: FTS brochure "Digital Currency Mining", rmo.nalog.gov.ru.

Step 3. Confirm contact details

After authorisation, the service will ask you to confirm your email and phone number.

Step 4. Create an application

In the "My applications" section you need to click "Create application". The service will ask you to confirm consent to the processing of personal data and to fill in basic information about the legal entity or sole proprietor. Some data is pulled automatically from the Unified State Register of Legal Entities or Sole Proprietors.

At this stage it is important to choose the correct application type: for a person engaged in digital currency mining, or for a mining infrastructure operator. These are different legal statuses, with different sets of information and different obligations. Check that the profile displays correct details of the applicant, the electronic signature holder and the organisation or sole proprietor on whose behalf the application is filed: a mistake at this stage can lead to refusal, additional requests or the need to re-file the application.

Step 5. Fill in the details

The application is divided into several stages. Depending on the applicant's status, the following may be required:

- information about the applicant;

- information about the website;

- information about officers;

- information about beneficial owners — i.e. persons who directly or indirectly own the legal entity or are able to control its actions;

- addresses where equipment is located;

- information about the mining infrastructure;

- supporting documents;

- signing and submission of the application.

For a mining infrastructure operator the set of information is broader, because the operator provides infrastructure for hosting other people's equipment. For a miner, the focus is on who carries out the mining, where the equipment is located, and how the obligation to report the digital currency received will be fulfilled.

If a miner files the application independently and operates without engaging a mining infrastructure operator, a contract with a grid company, an energy supply company or another document confirming the power supply of the mining facility may be required.

Step 6. Sign with a QES and submit

Once completed, the application is signed with a QES and submitted through the service. After submission, the application receives a unique identifier and the service shows the processing status. For example, the status "Receipt issued" means the request has been accepted for processing.

The FTS review period for the application is no more than 15 business days from the date of submission. The FTS may suspend the review once, for no more than 10 business days. The same period applies to an application for entry into the register of mining infrastructure operators.

How we do this for the client

When equipment is hosted with us, registration and organisational support may be part of the hosting package. What is included:

- preparation of the list of documents tailored to the client;

- review of the chosen model: the client as an independent miner, NODA as a support contractor, the mining infrastructure operator of the site, as well as a mixed model involving several parties within the project;

- completing the application in the FTS service;

- checking the information before submission;

- support with signing the application;

- monitoring the status until the result is obtained;

- help with preparing data for subsequent reporting.

If the application is filed through a mining infrastructure operator, we check in advance that the corresponding right is expressly set out in the contract with the miner and that the contract itself can be attached to the application. The application is signed with the QES of the applicant or of its authorised representative holding properly executed authority.

Preparing the package and completing the application, once all the data is received, usually takes 1–2 business days. The FTS review period is set by law and does not depend on NODA.

In plain terms: we take on the legal and organisational routine, but we do not replace the taxpayer where, by law, the obligations remain with the client. You get not just space for equipment, but a clear perimeter: a site, documents, registration support, data for reporting and a single point of communication.

Taxes and reporting for a register participant

Since 1 January 2025, dedicated tax regulation of transactions with digital currency, including mining, has been in effect. The main provision is Article 282.3 of the Tax Code. The key things to know:

- Legal entities. The tax base for transactions with digital currency is determined separately from the general corporate profit tax base. Mining income is calculated based on the market quotation of the digital currency on the date the income is recognised, applying the rouble-conversion rules. Expenses may be taken into account where they are documented and where the requirements of the Tax Code are met.

- Sole proprietors. Mining income is subject to personal income tax (PIT) under special rules. The exact calculation depends on the status, the amount of income, the expenses and the chosen activity model.

- Individuals. If an individual mines within the permitted energy-consumption limit and is not required to join the register, the income must still be declared in the established manner.

The special PIT scale for mining income:

- up to RUB 2.4 million per year — 13%;

- from RUB 2.4 to 5 million — 15%;

- from RUB 5 to 20 million — 18%;

- from RUB 20 to 50 million — 20%;

- over RUB 50 million — 22%.

The higher rate applies not to the entire amount of income, but to the portion of the tax base above the relevant threshold.

Special tax regimes. Payers under the simplified tax system (USN), the unified agricultural tax (ESHN), the automated simplified system (AUSN) and the professional income tax (NPD) are not entitled to apply those regimes if they carry out the issuance and subsequent sale of digital currency. So before launching mining through an existing sole proprietorship or LLC on a special regime, the tax model must be checked separately. Sometimes a separate legal entity, a separate accounting policy, separate accounting and a different contractual structure will be required.

VAT. Receiving digital currency through mining, and transactions with digital currency, are generally not subject to VAT. But this does not mean the whole project is "VAT-free": equipment hosting services, the supply of miners, technical maintenance, the data centre and other related services may have their own tax consequences, including VAT.

Reporting. A person engaged in digital currency mining reports to the FTS information about the digital currency received and about the identifier addresses. Under RF Government Decree No. 1466, the information is submitted no later than the 20th day of the month following the month in which the digital currency was received. In the cases and manner provided for by law, the information may be shared between authorised bodies, including Rosfinmonitoring and the Bank of Russia. It is therefore important that the data on mining, taxes, wallets and contracts do not contradict each other.

In plain terms. Received BTC through mining — you need to determine the income at the market quotation on the date the income is recognised. If the quotation is in a foreign currency, it is converted into roubles at the Central Bank of Russia rate. Sold the digital currency later — that is a separate transaction, whose tax consequences are calculated under the rules of the Tax Code.

A note for those who planned to operate under the USN. Before dedicated regulation appeared, many miners counted on a simple tax model. Doing so is now risky: if you have a legal entity on the USN and part of your activity involves mining, you should separate the activity types, tax bases, contracts, accounting and cash flows in advance.

What you face for illegal mining

This is the section many people read this post for.

As of 20 May 2026, dedicated provisions of the Code of Administrative Offences and the Criminal Code on liability specifically for illegal mining have not entered into force. At the same time, the bill on administrative liability for violations in the mining sphere has already passed its first reading, and the bill on criminal liability for illegal mining and for the illegal activity of a mining infrastructure operator has been recommended by the relevant State Duma committee for adoption in the first reading. Therefore, fines and criminal liability cannot be described as already applicable sanctions — but they must be taken into account as an imminent regulatory risk.

This does not mean that illegal mining is safe. Risks may arise in several directions:

- tax claims, if mining income is not declared or is understated;

- claims over energy consumption, if equipment is connected improperly or the wrong tariff is used;

- risks under the energy supply contract, lease, or operation of the premises or site;

- risks under Federal Law No. 115-FZ and banking compliance, if the origin of digital currency and funds is not confirmed;

- general administrative or criminal-law risks, if the actions contain elements of the relevant offence.

Seizure or confiscation of equipment is possible only where there are grounds provided for by law and in the established procedural order. It is not an automatic consequence of any violation.

In plain terms. The main risk of grey-zone mining today lies not only in a specific article of the Administrative or Criminal Code. The risk is that the activity becomes visible to power utilities, the tax authorities, banks and law enforcement — while the equipment owner has no proper package of documents, registration, reporting, tax accounting or a clear model.

Frequently asked questions

Can I mine without the register if I have one ASIC at home?

Yes, if you are an individual — a Russian citizen — are not a sole proprietor, and do not exceed the limit of 6,000 kWh per month. A single S21 Pro usually fits within this limit. The income must still be declared.

How much does registration cost — is there a state fee?

Filing the application through the FTS service does not involve a separate state fee. Costs may arise for the QES, accounting support, a legal review of the model, document preparation and support with filing the application. When hosting with NODA, we can include organisational support for registration in the hosting package.

Can I mine under the USN or PSN?

Mining cannot be safely treated as ordinary activity on a special tax regime. Payers under the USN, ESHN, AUSN and NPD are not entitled to apply those regimes if they carry out the issuance and subsequent sale of digital currency. If you already have a sole proprietorship or LLC on a special regime, the tax model must be checked separately before launching mining. Sometimes a separate legal entity, a separate accounting policy, separate accounting and a different contractual structure will be required.

Can I register retroactively for BTC already mined?

You cannot register retroactively. You may consider declaring previously received income through the tax procedure, but this does not guarantee the absence of questions from the tax authorities. The risks depend on the period, the volume of transactions, the documents, the source of electricity, the status of the person and the actual activity model.

Can I use a foreign company, for example in Cyprus, the UAE or Kazakhstan?

Using a foreign company does not, in itself, exempt you from Russian requirements if the computations are in fact performed on Russian territory. In such a model you need to analyse separately: who owns the equipment, where it is located, who receives the digital currency, who pays for electricity, who bears the tax obligations, whether there is a permanent establishment, currency risks, banking compliance, and the requirements of Russian mining regulation. The simple formula "register it to a foreign company and escape the Russian rules" does not work.

What counts as cloud mining and is the register required there?

Cloud mining models require separate analysis. If the user does not own the equipment, does not operate it, does not participate in a mining pool and in fact buys a financial or investment product, the obligation to join the register may be absent. But the model itself may carry other risks: investment, consumer-protection, tax, advertising, currency and banking risks. So there is no universal answer "the register is not needed" here — you need to look at the contract and the actual mechanics.

What should I do if my equipment is in a restricted region?

Stop mining or move the equipment to a region where the ban does not apply. Before relocating, check the current version of RF Government Decree No. 1869, because the list of territories and the timing of restrictions may change. If you need a site in a permitted region with ready infrastructure, we host equipment in Perm Krai.

Host your equipment with us

Host your equipment with NODA: we will help with infrastructure, documents, registration support and the preparation of data for reporting. We do not promise to "take on the client's taxes" where the client remains the taxpayer — but we can build a clear legal model, prepare documents, support registration and help organise further interaction with the FTS within the scope of the contract.

If, in your model, the application can be filed by a mining infrastructure operator, we will check the contractual basis in advance and prepare wording that allows this to be done correctly. If the client remains an independent miner, we will help collect the documents and data for an independent filing.

Request a specification and a payback calculation — leave a hosting request, write to contact@nodagroup.ru or message @nodasalesbot on Telegram. If you first need to choose miners and GPU servers — the catalogue has models with a payback calculation.

Announcements of upcoming posts on regulation, equipment and gas-fired energy are in our @nodagrid channel. Next analysis: how we calculate the break-even BTC price on our own gas-fired generation versus the grid tariff.

Disclaimer. This material is for information purposes only and does not constitute legal, tax, financial or investment advice. It is also not a public offer within the meaning of Article 437 of the Russian Civil Code. Before launching mining, registering in the register, choosing a tax model or hosting equipment, you must separately verify the applicable requirements in the light of your actual model, region, taxpayer status, contracts, source of electricity and volume of transactions.